Popular on s4story

- Acuvance Appoints Sandeep Sabharwal to Board of Directors, Strengthening Leadership to Support Continued Platform Growth - 128

- Sutra House Publishes Return of the Mary Celeste by Stephen Hayes - 115

- One Man's Harsh Quest for Redemption in Britain's Post-Apocalyptic Wasteland: New Thriller Out Now

- Resident Inspect Joins Property Meld Nexus Network with API Integration

- RAATV Premieres Original Reality Series "The Access Index: Jackson" June, 19

- Former CTO and Basketball Coach Launches Diagnostic "Mental Toughness" Workbook for Teens

- RAS AP Consulting Advances to RFP Stage in Heidelberg Materials' SAP Vendor & Customer Master Data Modernization Initiative

- Umbrella Becomes First FinOps Platform to Support AWS Billing Transfer Onboarding

- Virginia Moving Company Nearly Doubles Customer Calls in Two Weeks After Switching to CARL — the Bold New Alternative to WordPress

- HRC Fertility's Dr. Christo G. Zouves Appointed to San Mateo County Medical Association Board of Directors

Similar on s4story

- DLT Resolution, Inc. (Stock Symbol: DLTI) Expands Into the $224 Billion Life Settlements Market While Accelerating Telecom Growth Across Canada

- @tickerbitcoinbb and @girl_still_cute Announce the Arrival of SPROTO AEON BABY 1.0 – A New Chapter for the HarryPotterObamaSonic10Inu Universe

- XMax Inc. (N A S D A Q) Accelerates AI Expansion With $4.8 Million Contracted Revenue, $30+ Million Enterprise Pipeline and Strategic SpaceX Exposure

- RAS AP Consulting Advances to RFP Stage in Heidelberg Materials' SAP Vendor & Customer Master Data Modernization Initiative

- Free Critical Illness Claim Calculator Launches to the Public

- HealthBook+ and Stonebrook Risk Solutions Partner to Bring Predictive Intelligence to Healthcare Risk

- Umbrella Becomes First FinOps Platform to Support AWS Billing Transfer Onboarding

- NRx Pharmaceuticals (N A S D A Q: NRXP) Accelerates Into National Spotlight as Manufacturing Launch, Federal Policy & AI-Driven Breakthroughs Converge

- Expanding Into High-Margin Battery Recycling With Black Mass Strategy plus Scaling AI Infrastructure & Global Supply Chain Platform: N A S D A Q: MWYN

- 62% of Gen X have no estate planning documents — Trust & Will research identifies "the Sandwich Gap"

First Bancorp of Indiana, Inc. Announces Financial Results - March 31, 2026

S For Story/10692479

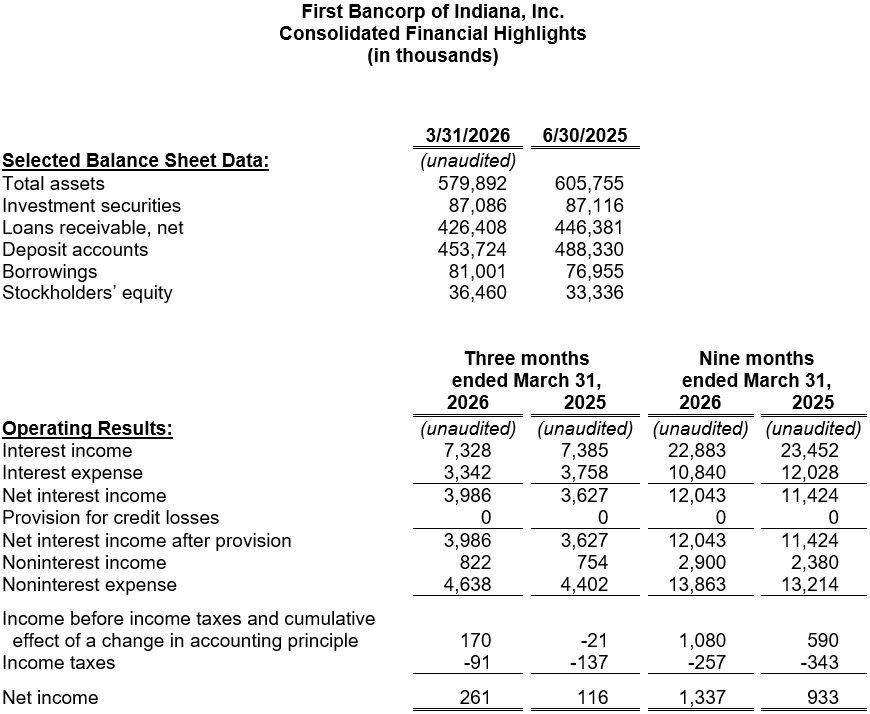

EVANSVILLE, Ind. - s4story -- First Bancorp of Indiana, Inc. (OTCPK:FBPI), the holding company (the "Company") for First Federal Savings Bank (the "Bank"), reported earnings of $261,000 ($0.15 per diluted common share) for the third fiscal quarter ended March 31, 2026, compared to $116,000 ($0.07 per diluted common share) for the same quarter a year ago. Likewise, earnings for the first three quarters of Fiscal 2026 totaled $1.34 million ($0.78 per diluted common share), compared to $933,000 ($0.55 per diluted common share) last fiscal year-to-date. Earnings for the nine-month period equate to a return on average assets ("ROAA") of 0.30% and a return on average equity ("ROAE") of 4.94%. This compares to an annualized ROAA of 0.20% and an annualized ROAE of 3.75% last fiscal year.

"Asset quality improved meaningfully compared to last year, reflecting the benefit of proactive borrower engagement and consistent credit administration oversight. We remain focused on early identification of risk and timely resolution strategies. We continued to strengthen our capital position this quarter through disciplined balance sheet management. Maintaining strong capital remains a priority as we focus on long-term stability and sustainable performance," stated Michael H. Head, President and CEO.

Net interest income for the quarter ended March 31, 2026, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), measured as a percentage of average interest-earning assets, was 2.97% for the quarter ended March 31, 2026, an improvement from 2.60% as reported for the same timeframe last year. Noninterest income increased during the most recent quarter, driven by improved service charges and higher interchange income. Noninterest expense also rose, primarily due to higher compensation costs and increased advertising related to a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $87.1 million on March 31, 2026, reflecting a modest decline since the beginning of the fiscal year.

Net loans outstanding, which totaled $426.4 million on March 31, 2026, have declined $20.0 million during the fiscal year chiefly due to the annual repayment of a cyclical loan relationship. Commercial loan production increased to $33.7 million for the first nine months of the fiscal year, including one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, totaled $15.8 million during the same timeframe. Construction lending represented 6.9% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $12.5 million.

More on S For Story

No provision for credit losses on loans was recorded in the nine months ended March 31, 2026 or 2025. Net loan recoveries totaled $44,400 for the first three quarters of the fiscal year, compared to $233,000 of charge offs for the comparative quarters last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.33% on March 31, 2026, compared to 1.94% a year ago, primarily as the result of the successful restructuring of two large commercial relationships.

Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.36 million at March 31, 2026, compared to $5.41 million on March 31, 2025. The portion of the allowance attributed to the loan portfolio represented 1.17% of at-risk loans on March 31, 2026, compared to 1.12% last year. Management considers the allowance sufficient under current conditions but acknowledges that ongoing economic uncertainty and elevated inflation – characteristics of the current economic cycle – could negatively impact the credit quality of the loan portfolio. In response, management continues to closely monitor borrowers most affected by these challenges and stands ready to adjust the allowance as needed to address emerging risks.

Deposit accounts, totaling $453.7 million on March 31, 2026, declined by $34.6 million since the beginning of the fiscal year. Seasonal variations in a large deposit relationship, coupled with the retirement of $37.8 million of higher-costing wholesale funding, account for the variance. Local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.34% for the current quarter compared to 2.56% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.50% for the quarter, compared to 2.69% for the quarter ended March 31, 2025.

As a part of the Bank's liquidity management plan, diversified contingency funding sources are maintained and liquidity stress tests are used to assess adequacy. At March 31, 2026, First Federal Savings Bank had unused lines of credit totaling $21.0 million available at correspondent financial institutions. Additional secured borrowing capacity is accessible from the Federal Reserve Bank's discount window ($20.9 million) and the Federal Home Loan Bank ($73.0 million).

Stockholders' equity totaled $36.5 million as of March 31, 2026, including a $7.7 million fair value adjustment to the available-for-sale securities portfolio. This adjustment is not included in regulatory capital calculations, and gains or losses in the securities portfolio are recognized in earnings only if a security is sold. Based on the 1,707,291 outstanding common shares on March 31, 2026, the book value per share of FBPI stock was $21.36, compared to $19.37 on March 31, 2025.

More on S For Story

On March 31, 2026, First Federal Savings Bank's Community Bank Leverage Ratio ("CBLR") stood at 9.38%. Comparatively, the Bank's Tier 1 Leverage ratio was 8.81% one year ago.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

"Asset quality improved meaningfully compared to last year, reflecting the benefit of proactive borrower engagement and consistent credit administration oversight. We remain focused on early identification of risk and timely resolution strategies. We continued to strengthen our capital position this quarter through disciplined balance sheet management. Maintaining strong capital remains a priority as we focus on long-term stability and sustainable performance," stated Michael H. Head, President and CEO.

Net interest income for the quarter ended March 31, 2026, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), measured as a percentage of average interest-earning assets, was 2.97% for the quarter ended March 31, 2026, an improvement from 2.60% as reported for the same timeframe last year. Noninterest income increased during the most recent quarter, driven by improved service charges and higher interchange income. Noninterest expense also rose, primarily due to higher compensation costs and increased advertising related to a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $87.1 million on March 31, 2026, reflecting a modest decline since the beginning of the fiscal year.

Net loans outstanding, which totaled $426.4 million on March 31, 2026, have declined $20.0 million during the fiscal year chiefly due to the annual repayment of a cyclical loan relationship. Commercial loan production increased to $33.7 million for the first nine months of the fiscal year, including one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, totaled $15.8 million during the same timeframe. Construction lending represented 6.9% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $12.5 million.

More on S For Story

- SpeedyIndex Rolls Out Automated API for Mass URL Verification, Solving the Backlink Blind Spot for SEO Agencies

- Michigan Attorney General Closed FGM Licensing Investigations Months Before Federal Case Ended, Records Show

- Mensa Foundation Event Reframes Brain Health for Every Age

- New from Regal House Publishing, Into the Night Woods, a boy's heroic effort to save his best friend

- DLT Resolution, Inc. (Stock Symbol: DLTI) Expands Into the $224 Billion Life Settlements Market While Accelerating Telecom Growth Across Canada

No provision for credit losses on loans was recorded in the nine months ended March 31, 2026 or 2025. Net loan recoveries totaled $44,400 for the first three quarters of the fiscal year, compared to $233,000 of charge offs for the comparative quarters last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.33% on March 31, 2026, compared to 1.94% a year ago, primarily as the result of the successful restructuring of two large commercial relationships.

Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.36 million at March 31, 2026, compared to $5.41 million on March 31, 2025. The portion of the allowance attributed to the loan portfolio represented 1.17% of at-risk loans on March 31, 2026, compared to 1.12% last year. Management considers the allowance sufficient under current conditions but acknowledges that ongoing economic uncertainty and elevated inflation – characteristics of the current economic cycle – could negatively impact the credit quality of the loan portfolio. In response, management continues to closely monitor borrowers most affected by these challenges and stands ready to adjust the allowance as needed to address emerging risks.

Deposit accounts, totaling $453.7 million on March 31, 2026, declined by $34.6 million since the beginning of the fiscal year. Seasonal variations in a large deposit relationship, coupled with the retirement of $37.8 million of higher-costing wholesale funding, account for the variance. Local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.34% for the current quarter compared to 2.56% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.50% for the quarter, compared to 2.69% for the quarter ended March 31, 2025.

As a part of the Bank's liquidity management plan, diversified contingency funding sources are maintained and liquidity stress tests are used to assess adequacy. At March 31, 2026, First Federal Savings Bank had unused lines of credit totaling $21.0 million available at correspondent financial institutions. Additional secured borrowing capacity is accessible from the Federal Reserve Bank's discount window ($20.9 million) and the Federal Home Loan Bank ($73.0 million).

Stockholders' equity totaled $36.5 million as of March 31, 2026, including a $7.7 million fair value adjustment to the available-for-sale securities portfolio. This adjustment is not included in regulatory capital calculations, and gains or losses in the securities portfolio are recognized in earnings only if a security is sold. Based on the 1,707,291 outstanding common shares on March 31, 2026, the book value per share of FBPI stock was $21.36, compared to $19.37 on March 31, 2025.

More on S For Story

- Indie Author Releases Dark Superhero Comedy and Suspense Tale

- Ashley Wineland's 'Love + Heartbreak' Tour Brings her Emotional and Empowering Album 'Wineland' to Nationwide Audiences

- People & Stories/Gente y Cuentos Welcomes Two New Trustees as Organization Enters 54th Year and Expands Community Reach

- At 59, Audrey Bell-Kearney Trades "Retirement Plans" for AI Murder

- Announcing The Stormlamp Rituals—An Illustrated Puzzle Book Launching on Kickstarter June 2nd

On March 31, 2026, First Federal Savings Bank's Community Bank Leverage Ratio ("CBLR") stood at 9.38%. Comparatively, the Bank's Tier 1 Leverage ratio was 8.81% one year ago.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

Source: First Bancorp of Indiana Inc

0 Comments

Latest on S For Story

- New Graphic Novel Playing With Knives Captures the Chaos of the 1980s Underground Rave Scene

- Slotozilla Expands Bonus Portfolio and Affiliate Reach Following iGB Barcelona 2026

- New from Regal House Publishing, This Impossible Vertical World

- The Periodical, NYC-Based Art and Literary Magazine, Launches

- XMax Inc. (N A S D A Q) Accelerates AI Expansion With $4.8 Million Contracted Revenue, $30+ Million Enterprise Pipeline and Strategic SpaceX Exposure

- Lnk.Bio Becomes the First Link-in-Bio Service Fully Manageable from Inside ChatGPT

- Tenebroso Earns Glowing Review from Readers' Favorite

- Did Drake Just Find His Next Signee? Peoria Rapper Rhymi Gifts "ICEMANDRAKE" Domains, Drops Debut Album Same Day

- The Letter That Should Have Changed The World

- Andrew Tate Says Los Angeles Is "Where I Belong" as He Hints at USA Move

- RAS AP Consulting Advances to RFP Stage in Heidelberg Materials' SAP Vendor & Customer Master Data Modernization Initiative

- Expert E-Bike Safety Advocate Issues Urgent Warning Following Recent Southern California Fatalities

- VeneerVibe Releases 2026 Snap-On Veneers Market Report

- David Cavanagh Launches AI SEO Company For ChatGPT And AI Search Visibility

- Minnesota Author Gopu Shrestha Launches 7-Book Collection on Leadership, Agile and AI

- Matthew Cossolotto Spotlights Make a Promise Day 2026 Events, Including Official Launch of Harness Your PromisePower and Issuing a "Peace Promise"

- New Book - The Flip Economy Playbook - Reveals How Everyday Items Can Turn Into Real Profit in 2026

- Community Comes Together for Earth Day Clean-Up in Commerce

- Landmark Expands Services to Include Specialized Glass and Glazing Solutions Across Los Angeles

- As Pentagon Releases Ufo Files, Debut Ya Novel Predicted It All