Popular on s4story

- Libraries for Kids International Announces 2026 Board of Directors - 211

- For Valentine's Day: Treat yourself (and maybe even your sweetheart) to some Not Exactly Love Poems - 111

- OneVizion Announces Next Phase of Growth as Brad Kitchens Joins Board of Directors

- Power Business Solutions Announces Joint Venture with EIG Global Trust to Deliver Data Center Financial Solutions

- Michael Judkins Releases New Poetry Book, Deeper Than You Think

- Donna L. Quesinberry, President of DonnaInk Publications, Unveils New Article on Author Monetization

- Scoop Social Co. Partners with Fairmont Hotels & Resorts to Elevate Summer Guest Experiences with Italian Inspired Gelato & Beverage Carts

- "They Said It Was Impossible": This Bottle Turns Any Freshwater Source Into Ice-Cold, Purified Drinking Water in Seconds

- DonnaInk Publications Announces Powerful First-half of 2026 Release Slate

- The Myth of Atlantis, Reconsidered Through Forbidden Texts

Similar on s4story

- FDA Meeting Indicates a pivotal development that could redefine the treatment landscape for suicidal depression via NRx Pharmaceuticals: $NRXP

- $2.7 Million 2025 Revenue; All Time Record Sales Growth; 6 Profitable Quarters for Homebuilding Industry: Innovative Designs (Stock Symbol: IVDN)

- Slotozilla Reports Strong Q4 Growth and Sigma Rome Success

- Why KULR Could Be a Quiet Enabler of Space-Based Solar Power (SBSP) Over The Long Term: KULR Technology Group, Inc. (NY SE American: KULR)

- Why Finland Had No Choice But to Legalize Online Gambling

- High-Margin Energy & Digital Infrastructure Platform Created after Merger with Established BlockFuel Energy, Innovation Beverage Group (NAS DAQ: IBG)

- Municipal Carbon Field Guide Launched by LandConnect -- New Revenue Streams for Cities Managing Vacant Land

- Aleen Inc. (C S E: ALEN.U) Advances Digital Wellness Vision with Streamlined Platform Navigation and Long-Term Growth Strategy

- RimbaMindaAI Officially Launches Version 3.0 Following Strategic Breakthrough in Malaysian Market Analysis

- Fed Rate Pause & Dow 50k: Irfan Zuyrel on Liquidity Shifts, Crypto Volatility, and the ASEAN Opportunity

First Bancorp of Indiana, Inc. Announces Financial Results December 2025

S For Story/10684756

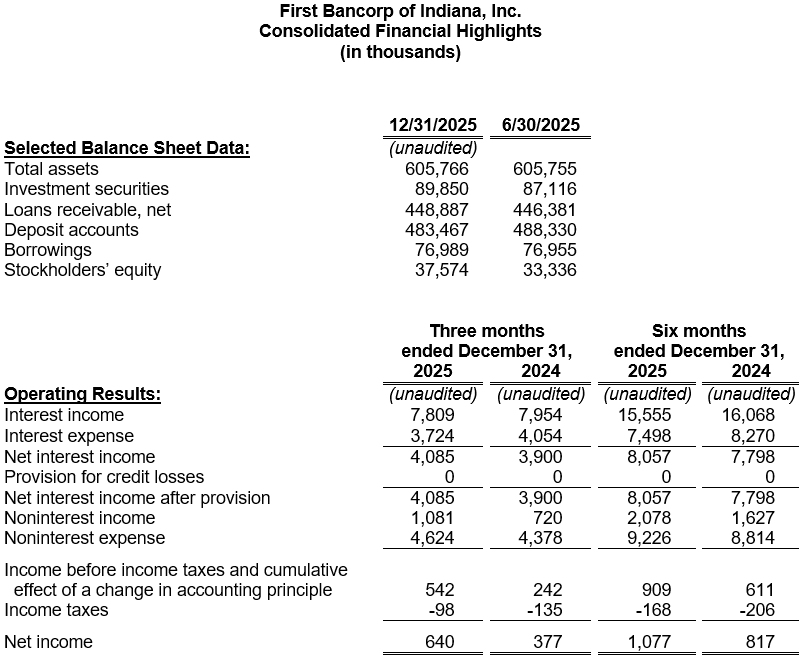

EVANSVILLE, Ind. - s4story -- First Bancorp of Indiana, Inc. (OTCPK:FBPI), the holding company (the "Company") for First Federal Savings Bank (the "Bank"), reported earnings of $640,000 ($0.38 per diluted common share) for the second fiscal quarter ended December 31, 2025, compared to $377,000 ($0.22 per diluted common share) for the same quarter a year ago. Likewise, earnings for the first half of Fiscal 2026 totaled $1.08 million ($0.63 per diluted common share), compared to $817,000 ($0.48 per diluted common share) last fiscal year-to-date. Earnings for the six-month period equate to a return on average assets ("ROAA") of 0.36% and a return on average equity ("ROAE") of 6.14%. This compares to an annualized ROAA of 0.26% and an annualized ROAE of 4.92% last fiscal year.

"Our second fiscal quarter results reflect meaningful progress in strengthening earnings performance," stated Michael H. Head, President and CEO. "The improvement in returns on assets and equity underscores the benefits of our continued focus on disciplined growth, expense management, and balance sheet optimization."

Net interest income for the quarter ended December 31, 2025, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.88% for the six months ended December 31, 2025, an improvement from 2.66% as reported for the same timeframe last year. Noninterest income increased during the most recent quarter as gains on loan sales accelerated and a gain on a life insurance claim was recognized. The quarter over quarter rise in total non-interest expenses was largely attributed to higher compensation expense due to annual merit increases and to advertising costs from a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $89.9 million on December 31, 2025. No investments were added, so the modest increase was attributed to an improvement in the portfolio's fair market value, net of scheduled repayments.

Net loans outstanding, which totaled $448.9 million on December 31, 2025, have increased $2.5 million during the fiscal year. Commercial loan production totaled $23.4 million for the first half of the fiscal year, which included one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, increased to $12.0 million during the same timeframe. Construction lending accounted for 9.1% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $9.0 million.

More on S For Story

No provision for credit losses on loans was recorded in the six months ended December 31, 2025 or 2024. Net loan recoveries totaled $48,200 for the first two quarters of the fiscal year, compared to $75,800 of charge offs for the comparative quarters last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.22% on December 31, 2025, compared to 1.76% a year ago, primarily as the result of the successful restructuring of two large commercial relationships.

Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.36 million at December 31, 2025, compared to $5.57 million on December 31, 2024. The portion of the allowance attributed to the loan portfolio represented 1.15% of at-risk loans on December 31, 2025, compared to 1.14% last year. Management considers the allowance sufficient under current conditions but acknowledges that ongoing economic uncertainty and elevated inflation – characteristics of the current economic cycle – could negatively impact the credit quality of the loan portfolio. In response, management continues to closely monitor borrowers most affected by these challenges and stands ready to adjust the allowance as needed to address emerging risks.

Deposit accounts, totaling $483.5 million on December 31, 2025, declined by $4.9 million from the beginning of the fiscal year. The reduction was attributed to growth in local deposits that allowed the Bank to retire $31.7 million of higher-costing wholesale funding. Local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.51% for the current quarter compared to 2.62% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.65% for the quarter, compared to 2.76% for the quarter ended December 31, 2024.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At December 31, 2025, First Federal Savings Bank maintained lines of credit totaling $25.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($6.7 million) and the Federal Home Loan Bank ($82.4 million).

Stockholders' equity reached $37.6 million as of December 31, 2025. This figure reflects a $6.5 million fair value adjustment to the available-for-sale securities portfolio, which improved due to the recent decline in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized if a security is sold. Based on the 1,707,291 outstanding common shares on December 31, 2025, the book value per share of FBPI stock was $22.01, compared to $19.39 on December 31, 2024.

More on S For Story

On December 31, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios were 8.96%, 13.01%, and 14.26%, respectively - improvements from 8.41%, 12.12% and 13.36% on December 31, 2024.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

"Our second fiscal quarter results reflect meaningful progress in strengthening earnings performance," stated Michael H. Head, President and CEO. "The improvement in returns on assets and equity underscores the benefits of our continued focus on disciplined growth, expense management, and balance sheet optimization."

Net interest income for the quarter ended December 31, 2025, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.88% for the six months ended December 31, 2025, an improvement from 2.66% as reported for the same timeframe last year. Noninterest income increased during the most recent quarter as gains on loan sales accelerated and a gain on a life insurance claim was recognized. The quarter over quarter rise in total non-interest expenses was largely attributed to higher compensation expense due to annual merit increases and to advertising costs from a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $89.9 million on December 31, 2025. No investments were added, so the modest increase was attributed to an improvement in the portfolio's fair market value, net of scheduled repayments.

Net loans outstanding, which totaled $448.9 million on December 31, 2025, have increased $2.5 million during the fiscal year. Commercial loan production totaled $23.4 million for the first half of the fiscal year, which included one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, increased to $12.0 million during the same timeframe. Construction lending accounted for 9.1% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $9.0 million.

More on S For Story

- Arbutus Medical Raises C$9.3M to Accelerate Growth of Surgical Workflow Solutions Outside the OR

- From Sleepless Nights to Sold-Out Drops: Catch Phrase Poet's First Year Redefining Motivational Urban Apparel

- Launching at 10AM Eastern: The Bottle That Chills and Purifies Any Water — No Ice Required

- How Specialized Game Development Services Are Powering the Next Wave of Interactive Entertainment

- Words of Veterans Honors Presidents Day with State-Supported Effort to Preserve Veteran Stories

No provision for credit losses on loans was recorded in the six months ended December 31, 2025 or 2024. Net loan recoveries totaled $48,200 for the first two quarters of the fiscal year, compared to $75,800 of charge offs for the comparative quarters last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.22% on December 31, 2025, compared to 1.76% a year ago, primarily as the result of the successful restructuring of two large commercial relationships.

Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.36 million at December 31, 2025, compared to $5.57 million on December 31, 2024. The portion of the allowance attributed to the loan portfolio represented 1.15% of at-risk loans on December 31, 2025, compared to 1.14% last year. Management considers the allowance sufficient under current conditions but acknowledges that ongoing economic uncertainty and elevated inflation – characteristics of the current economic cycle – could negatively impact the credit quality of the loan portfolio. In response, management continues to closely monitor borrowers most affected by these challenges and stands ready to adjust the allowance as needed to address emerging risks.

Deposit accounts, totaling $483.5 million on December 31, 2025, declined by $4.9 million from the beginning of the fiscal year. The reduction was attributed to growth in local deposits that allowed the Bank to retire $31.7 million of higher-costing wholesale funding. Local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.51% for the current quarter compared to 2.62% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.65% for the quarter, compared to 2.76% for the quarter ended December 31, 2024.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At December 31, 2025, First Federal Savings Bank maintained lines of credit totaling $25.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($6.7 million) and the Federal Home Loan Bank ($82.4 million).

Stockholders' equity reached $37.6 million as of December 31, 2025. This figure reflects a $6.5 million fair value adjustment to the available-for-sale securities portfolio, which improved due to the recent decline in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized if a security is sold. Based on the 1,707,291 outstanding common shares on December 31, 2025, the book value per share of FBPI stock was $22.01, compared to $19.39 on December 31, 2024.

More on S For Story

- In Face of AI Job Disruption, Ex Tech Manager Chooses Uncertainty, Says 'Build Your Own Boat'

- Don't Settle for a Lawyer Who Just Speaks Spanish. Demand One Who Understands Your Story

- Dan Williams Promoted to Century Fasteners Corp. – General Manager, Operations

- Ski Johnson Inks Strategic Deals with Three Major Food Chain Brands

- NIL Club Advances Agent-Free NIL Model as Oversight Intensifies Across College Athletics

On December 31, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios were 8.96%, 13.01%, and 14.26%, respectively - improvements from 8.41%, 12.12% and 13.36% on December 31, 2024.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

Source: First Bancorp of Indiana Inc

0 Comments

Latest on S For Story

- Finland's €1.3 Billion Digital Gambling Market Faces Regulatory Tug-of-War as Player Protection Debate Intensifies

- The Door You Hold Open Explores Quiet Leaving, Burnout, and Life Between Identities

- Angels Of Dirt Premieres on Youtube, Announces Paige Keck Helmet Sponsorship for 2026 Season

- "They Said It Was Impossible": This Bottle Turns Any Freshwater Source Into Ice-Cold, Purified Drinking Water in Seconds

- Patron Saints Of Music Names Allie Moskovits Head Of Sync & Business Development

- Dave Aronberg Named 2026 John C. Randolph Award Recipient by Palm Beach Fellowship of Christians & Jews

- General Relativity Challenged by New Tension Discovered in Dark Siren Cosmology

- Unseasonable Warmth Triggers Early Pest Season Along I-5 Corridor

- Bug Busters Expands Service Footprint With New Carrollton, Georgia Branch

- Why KULR Could Be a Quiet Enabler of Space-Based Solar Power (SBSP) Over The Long Term: KULR Technology Group, Inc. (NY SE American: KULR)

- Why Finland Had No Choice But to Legalize Online Gambling

- High-Margin Energy & Digital Infrastructure Platform Created after Merger with Established BlockFuel Energy, Innovation Beverage Group (NAS DAQ: IBG)

- iFLO Pro Launches Its Groundbreaking iFLO Pro Mini At The 2026 AHR Expo In Las Vegas

- TL International Group Becomes First Global Operator to Fully Migrate to Pulsant's Dedicated Car Rental Cloud

- Diveroli Investment Group Files 13D in PetMed Express, Highlights Strategic Value, Asset Floor, and Multiple Takeover Pathways

- Deep Learning Robotics (DLRob) Announces Pre-Launch of Zero-Teach and Teach-by-Demonstration Technology for Kitting Applications

- The Quasar Dipole Phenomenon is likely just a complex systematics artifact

- Soil Testing Matters for Healthy, Vibrant Rose Blooms

- The Rise of Comprehensive Home Water Treatment Systems

- Yazaki Innovations to Introduce First-Ever Prefabricated Home Wiring System to U.S. Residential Market in 2026